Property Analytics uses a cross-sectional factor-based approach to analyse the London real estate market, similar to those widely used in equity market analysis. This methodology allows us to decompose property returns into specific factors that drive market prices.

Factor Model Development

Our model was developed through rigorous statistical analysis of London property transaction data from 1995. We employed multiple regression techniques to identify the key factors that consistently explain variations in property prices across different market cycles.

A Cross-sectional model

Decomposing returns into factors can be done in mainly three ways: a purely statistical approach, time-series regression, and cross-sectional regression. The first one is hard to interpret, and the second one requires knowing the factor returns a priori. The third one is the most powerful and therefore widely used for stocks. All it requires is knowing the characteristics of each property and regressing the prices on those to derive the factor returns. Fortunately, this is very easy for properties where we can use, for example, the number of rooms, but it's somewhat harder for stocks.

Mathematical Model

At each month t, we fit a cross-sectional OLS of log(price/sqm) on property characteristics, each centred on its window mean X̄j,window — the mean of Xj over the transactions in the rolling 3-month window:

\[

y_i \;=\; \alpha_t \;+\; \sum_{j=1}^{k} \beta_{t,j}\bigl(X_{i,j} - \bar{X}_{j,\text{window}}(t)\bigr) \;+\; \varepsilon_i

\]

Centring makes the intercept αt interpretable as the log-price of the average transaction in the current window. Each βt,j is the premium paid per unit of characteristic j at time t.

The period-on-period change in quality-adjusted log-price decomposes via a first-order Taylor expansion evaluated at t:

\[

\Delta \hat{y}(t) \;=\; \Delta\alpha_t \;+\; \sum_{j=1}^{k} \Bigl[\underbrace{\beta_{t,j}\,\Delta X_j}_{\text{composition}} \;+\; \underbrace{X_j(t)\,\Delta \beta_{t,j}}_{\text{factor return}} \;-\; \underbrace{\Delta \beta_{t,j}\,\Delta X_j}_{\text{cross term}}\Bigr]

\]

The first two terms use current-period weights (βt, Xt). This is not an exact first-order decomposition of d(β·X) — it over-counts by Δβ·ΔX. We track that cross term explicitly as its own column in factor_returns.csv so the decomposition closes:

- Baseline Market = cumsum of Δαt + control-dummy contributions + factor composition effects

- Factor j = cumsum of Xj(t) · Δβt,j — the market's repricing of characteristic j at the current basket weight

- Cross Term = −cumsum of Σj Δβt,j·ΔXj — reconciles the non-exact split

By construction Baseline + Σ Factors + Cross Term exactly equals the cumulative change in ŷ(t). The cross term is usually small in practice (second-order in monthly changes) but is plotted explicitly on the Trends page so you can see the bias it would introduce under a naive current-values split.

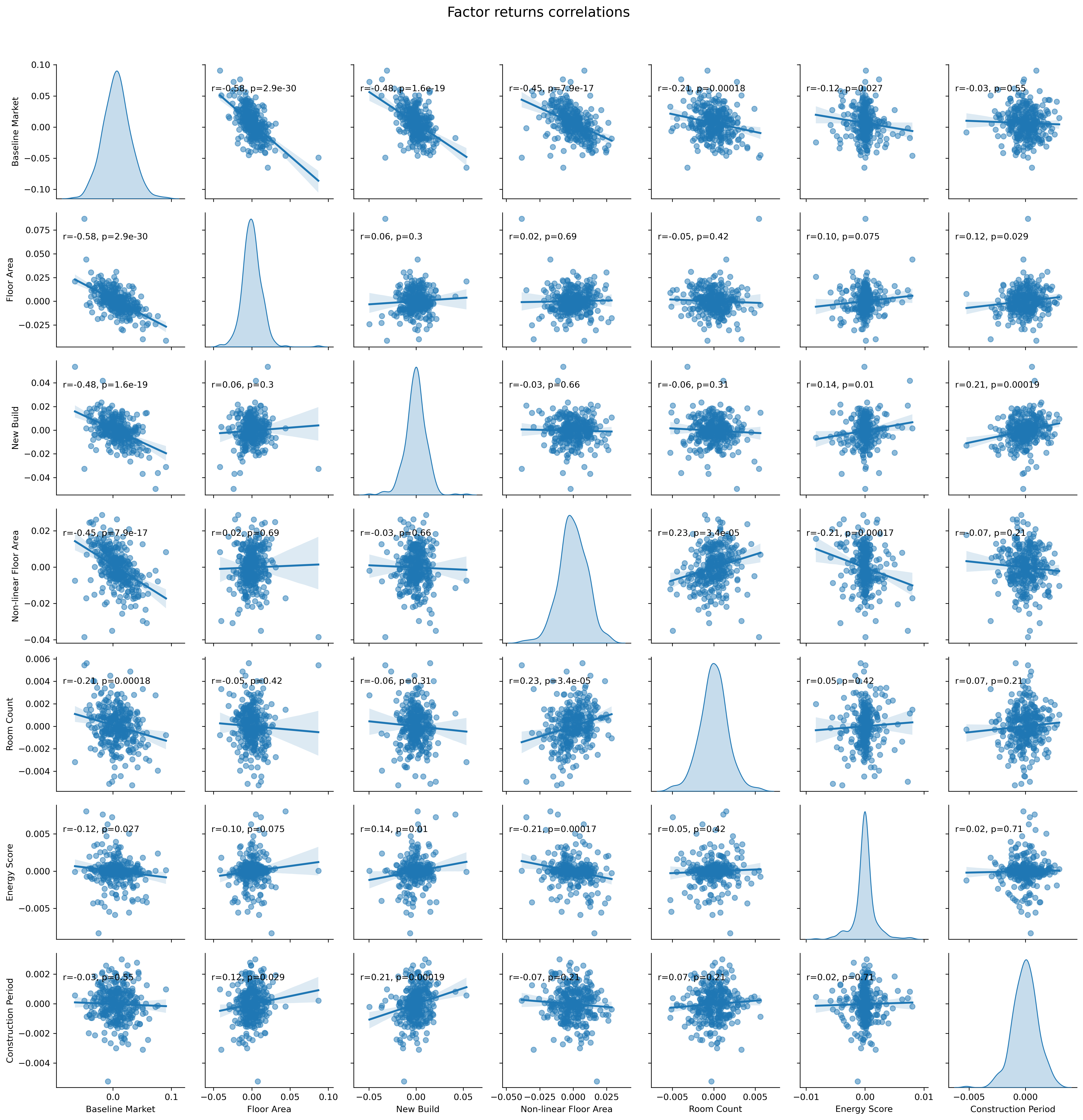

Factor Selection Process

We started with a comprehensive set of potential factors and systematically eliminated those with low explanatory power or high correlation with other factors. The final model includes 8 factors that collectively provide a robust framework for understanding London property prices:

- Baseline market return

- Total floor area

- New build premium

- Non-linear floor area

- Number of habitable rooms

- Energy efficiency

- Construction period

- Flat premium

Model Validation

We validate our model using rigorous statistical tests, like ratio between residuals and factor returns, low factor cross-correlations, and low autocorrelations. We also do out-of-sample testing, comparing its predictions against actual market transactions.